Warren Buffett of Berkshire Hathaway (BRK-A) (BRK-B) gave a speech to college graduates about how to succeed in business. It’s not about the money you start with.

Author: WSTNN

Hey Billionaires: If You Think That Taxes Should Be Raised for Billionaires, You Should …

by Fred Fuld III

The United States government has a huge amount of debt. As a matter of fact, the government debt now stands at more than $30,482,000,000,000.

One way to pay down that debt is through higher taxes. There are several billionaires that believe taxes on billionaires should be increased for themselves and other billionaires

Some of these wealthy individuals include:

- Warren Buffett

- Bill Gates

- George Soros

- Eli Broad

- Michael Bloomberg

- Mark Cuban

But what I can’t understand is that if the wealthy really believe this, what are they waiting for?

Billionaires that believe their taxes should be higher should go ahead and make more payments to the U.S. Government.

Nothing is stopping them. They can write a check out right now. Apparently, quite a few people have “donated” to the government.

There are actually a couple ways to make these payments to help reduce the national debt. Here is what they need to do:

They can go to Pay.gov, and pay online by credit card, debit card, PayPal, checking account, or savings account.

If they pay by credit card, I hope they have a nice high credit limit. Maybe they can earn points on their payments.

The other way is by writing a check, and make it payable to the Bureau of the Fiscal Service, and, in the memo section, notate that it is a gift to reduce the debt held by the public. The check should be mailed to:

Attn Dept G

Bureau of the Fiscal Service

P. O. Box 2188

Parkersburg, WV 26106-2188

So what are these billionaires waiting for? Why don’t they put their money where their mouth is?

10 Ways to Make Money in a Bear market

by Fred Fuld III

Although the stock market has been rising for the last several days, some investors and traders believe that this rise is only temporary, and that we are in the beginning of a bear market. If you want to profit from downward markets and falling prices, there are many ways to do so.

Several techniques are available to make money in a bear market, some of which are speculative, and some not that risky. Even if you have a small account, there are ways to protect yourself, and even make money on the downside. Here are some of those strategies.

1. Sell a Vertical Call Option Spread

This strategy is a little complicated, but I listed it first, because it is one of the least risky, since your losses are limited, unlike most of the other strategies listed here. Also, I listed it at the beginning, because I use this trading technique all the time.

If you are familiar with options, then selling a vertical call spread is a great way to make money when a stock drops while protecting yourself if the stock goes up. (This happens to be my favorite strategy.)

This involves shorting an out of the money call option and buying a further out of the money call option at the same time. If the stock drops or stays the same, you make money from the short call which exceeds the loss on the long call. If the stock goes up to the strike price of the short call, you still make a profit. It is only when the stock rises above the strike price of the short call that you begin losing money.

To make it simple, here is an example:

Stock is at 50

Sell (short) one call with a strike price of 51 for 3 (an option that is trading at 3 means $300)

Buy one call with a strike price of 52 for 1 ($100)

If the stock drops to 45, the 51 call drops to $0 and you make $300 because you shorted it, and the 52 call drops to $0 losing $100 because you own or were long it, netting you a profit of $200.

If the stock rises from 50 to 100, you lose $4900 on the 51 call that you shorted, but you make $4800 on the one that you bought, so you only lose $100.

Generally, you want to use options that expire in 40 to 60 days, and close out your position in 15 to 25 days.

Disadvantages of the selling a vertical call spread

- Your profit is limited

- You need approval from your broker to do option spreads

- Both legs of the spread need to be placed simultaneously (easy to do with most trading platforms)

- May need to wait 25 or 30 days to see a profit

2. Shorting Stocks

This is one of the most speculative ways of making money in a bear market. In simple terms, you make money when the stock goes down and you lose money when the stock goes up. What technically happens is that you borrow the shares and immediately sell them (this all is done electronically through your brokerage firm) and since you owe those shares, you eventually have to buy them back at some price, hopefully a lower price, in order to return those shares. The difference between your sale price and eventual purchase price is your profit (or loss, if you buy back at a higher price).

Can you make a lot of money shorting stocks in a bear market? Yes. Is it speculative? Very. Can you lose a lot? Most definitely. This is why it is so risky. When you short a stock, the lowest point it can drop to is zero. Whereas, if the stock goes up, the amount it can rise is unlimited. Let’s say you short 100 shares of a stock at $20 a share. If you put up funds equal to 100% of the value of the shorted amount, and the stock drops to zero, you’ve made a 100% return. However, suppose the stock goes from 20 to 100, you end up losing 400% of your money with lots of margin calls along the way. This is called a short squeeze. But even on a short term basis, an investor can lose money very fast.

Unfortunately for those who do their trading in retirement accounts, such as IRAs, shorting stocks is not allowed.

So in summery, do I think you should short stocks? Absolutely not, unless you are a professional trader. The risk is almost infinite. If you understand options real well, hedged short selling might be OK (see the next strategy), as long as you are an advanced trader, and know what you’re doing.

3. Hedged Short Selling

Hedged short selling is a strategy whereby you short a stock and at the same time, you buy a close-to-the-money call option. That way, if the stock shoots up, you are protected with the call option. If the stock drops, you will lose what you paid for the option, but you will make money on your short stock position.

Example: you short 100 shares of a stock that is currently trading at 50 (so you short $5000 in stock), and you buy a call option with a strike price of 52 for 1 ($100).

The stock goes to 40. You make $1000 from the stock dropping from 50 to 40, and you lose the $100 you paid for the call option, with a net profit of $900.

The stock stays the same at 50. You don’t make any money on the short sale fo the stock and you lose $100 on the call option for a net loss of $100.

The stock goes up to 60. You lose $1000 on the short stock, but the value of the call option will increase from 1 to 10 ($100 to $1000), netting $900 on the difference, for an overall loss of $100.

In other words, in the example above, you can only lose $100, if the stock stays the same or goes up, but if the stock drops, the profit can be substantial.

Actually, to be more accurate, if the stock goes to 51 and stays there, you will lose $100 on the short stock sale and $100 on the call option, for a total maximum loss of $200. Even still, it may be worth the small loss in case you are wrong about a bear market.

Disadvantages of the hedged short selling

- You need approval from your broker to short stock and buy options

- Both positions should be placed simultaneously (easy to do with most trading platforms)

4. Short (Bearish) ETFs

The Exchange Traded Fund known as the Bearish ETF or Short ETF is another option. What these ETFs do is provide a return opposite to the return of the index, sector, or industry that it is tracking.

For example, the Short Dow30 ProShares (DOG) provides a return that is the inverse of the Dow Jones Industrial Average. If the Dow goes down 2%, the DOG is expected to up 2%. The Short QQQ ProShares (PSQ) ETF gives a return that is the inverse of the NASDAQ 100 Index.

The nice thing about these short ETFs is that your losses are limited. Also, if you are long individual stocks that you don’t want to sell, these can be good for protecting your overall portfolio on the downside.

5. Leveraged Bearish ETFs

If you like volatility, you will love the leveraged bearish ETFs. What these ETFs do is provide double, and in some cases triple the inverse return of indices.Some examples include the UltraShort Consumer Services ProShares (SCC) and the ProShares UltraShort S&P S&P 500 (SDS).

In addition there are several triple leveraged bearish ETFs. Direxion Daily MCSI Real Estate Bear 3X Shares (DRV), Direxion Daily Energy Bear 2X Shares (ERY), and ProShares UltraPro Short Russell 2000 (SRTY) are just a few of the many leveraged bearish ETFs.

The volatility of these ETFs is substantial, and so are the wide bid and asked spreads that I’ve seen occasionally.

The advantage of these trading vehicles is that they are a way of shorting on margin, with a limit on the downside. The disadvantage is that the losses can be quick and large, especially with the triple leverage short ETFs.

6. Bear Funds

It may be hard to believe, but there are actually a large number of bearish mutual funds for the long term bearish investors. These include the Grizzly Short Fund (GRZZX), the PIMCO StocksPlus TR Short Strategy Institutional Fund (PSTIX), and the ProFunds Bear Investors Fund (BRPIX). These funds have minimum investments ranging from $1,000 to $5,000,000.

7. Puts

First, a little about option pricing. Puts and calls are priced on a per share basis, so a put at $1 would cost $100 for a 100 share option, or a call at $3.50 would cost $350.

A put is the option to put your stock to someone at a particular price within a certain period of time. In other words, if you own a stock that is trading at 22 and you buy a put at a dollar which gives you the right to put your stock to someone at $20 per share within three months, there are a couple of things that could happen. The stock could tank to $14 a share and you could put your stock at 20, or just resell the put for 6 (the difference between 14 and 20) and collecting the profit. You would be far better off than just doing nothing. And if the stock goes up or stays about the same, you are just out your $100 for the option. Puts can be useful for experienced traders.

8. Cash

There is one other way to make money in a bear market. Sell everything, and keep your money in cash, with the safest way being a T-bill money market fund, that only owns T-bills. (Money market funds that invest in repos are supposed to be just as safe, but I consider them slightly more risky than T-bills.) The advantages are that you can’t lose money and you can receive an income from the investment.

The alternative cash investment is putting your money in a bank certificate of deposit or savings account. Your money is safe up to the FDIC limits, but the interest rate will be very low.

9. Anti ETFs

The Anti-ETF is a new investment vehicle that has cropped up recently. The goal of these ETFs is to provide the reverse return of another popular actively managed exchange traded fund, as opposed to the bearish ETF which attempt to track the inverse of an index, like the ProShares Short S&P500 ETF (SH).

The most popular is the Tuttle Capital Short Innovation ETF (SARK), which has a goal of achieving the inverse of the return of the popular ARK Innovation ETF (ARKK) managed by Cathie Wood.

10. Series I Bonds

If you think the bear market will last for a year or more, Series I bonds are the way to go. These bonds never drop in value and currently pay 9.62%. Plus, they are backed by the U.S. Government. For more information on these bonds, check out the article Series I Bonds Now Paying over 9%.

There are obviously additional risks involved with shorting stock and options, which you need to delve into with your broker before utilizing those strategies. If we are in a bear market, hopefully you can protect your portfolio and make some money on the downside.

Author does not own any of the above mentioned securities.

Series I Bonds Now Paying Over 9%

by Fred Fuld III

How would you like to own the following investment:

- It currently pays 9.62%

- It is backed by the United States Government

- It has an inflation factor

- There is no commission

- You can own it either electronically or in paper form

- The interest is exempt from state and local income taxes

- Interest earnings may be excluded from Federal income tax when used to finance education

- The investment never drops in price

- There is no minimum investment (well almost no minimum, you can invest less than $100)

So what kind of investment is this? No, it is not Forever Stamps. Sound too good to be true? It is called the Series I Savings Bond.

Here are the details.

What is an I Bond?

A Series I savings bond is a security issued by the United States Government that earns interest based on both a fixed rate and a rate that is set twice a year based on inflation. The bond earns interest until it reaches 30 years or you cash it, whichever comes first.

What’s the interest rate on an I Bond I buy today?

For the first six months you own it, the Series I bond is currently paying interest at an annual rate of 9.62%. A new rate will be set every six months based on the bond’s fixed rate and on inflation.

Special Benefits of Series I Bonds

You can own a bond in the name of a living trust. I know, because I’ve done it. It will be tied to you Social Security number.

For those that want to invest a lot of money in these bonds, they need to be aware that there is a $10,000 limit per calendar year per person. So a married couple could buy $20,000 now. Then next January, they could buy another $20,000, for a total of $40,000 in less than a nine month period.

In addition, there is another way they could buy more. An additional $5,000 per year can be invested in Series I bonds, using their tax refund. If you haven’t done your taxes yet (like me; I filed an extension, and yes, I’m still getting 1099s in late May), and you are expecting a refund of over $5,000, then $5,000 can be applied towards I bonds.

For next year, if you aren’t anticipating a big refund, you can always overpay your taxes by $5,000 so that you can get the maximum amount in Series I bonds for next year.

So assuming all things are in place, a married couple could theoretically invest $50,000 in I bonds in less than a year.

Who may own an I Bond?

| Individuals | Yes, if you have a Social Security Number and meet any one of these three conditions:

To buy and own an electronic I bond, you must first establish a TreasuryDirect account. |

| Children under 18 | Yes, if they meet one of the conditions above for individuals. Information concerning electronic and paper bonds:

|

| Trust, estate, corporation, partnership and some other entities | Electronic bonds (in TreasuryDirect): Yes Paper bonds:

|

How can I buy I Bonds?

Two options:

- Buy them in electronic form in our online program TreasuryDirect

- Buy them in paper form using your federal income tax refund

What determines who owns an I Bond and who can cash it?

How you register the bond at purchase determines who owns the bond and who can cash it. The registration is the name of the owner (either a person or entity), the Taxpayer Identification Number, and, if applicable, the second-named owner or beneficiary.

What do I Bonds cost?

You pay the face value of the bond. For example, you pay $50 for a $50 bond. (The bond increases in value as it earns interest.)

Electronic I bonds come in any amount to the penny for $25 or more. For example, you could buy a $50.23 bond.

Paper bonds are sold in five denominations; $50, $100, $200, $500, $1,000

How much in I Bonds can I buy for myself?

In a calendar year, you can acquire:

- up to $10,000 in electronic I bonds in TreasuryDirect

- up to $5,000 in paper I bonds using your federal income tax refund

Two points:

- The limits apply separately, meaning you could acquire up to $15,000 in I bonds in a calendar year

- Bonds you buy for yourself and bonds you receive as gifts or via transfers count toward the limit. Two exceptions:

- If a bond is transferred to you due to the death of the original owner, the amount doesn’t count toward your limit

- If you own a paper bond issued before 2008, you can convert it to an electronic bond in your account in TreasuryDirect regardless of the amount of the bond. (The annual limit before 2008 was greater than today’s limit of $10,000.)

Can I buy I Bonds as gifts for others?

Yes.

Electronic bonds: You can buy them as gifts for any TreasuryDirect account holder, including children.

Paper bonds: You can request bonds in the names of others and then, once the bonds are mailed to you, give the bonds as gifts.

How much in I Bonds can I buy as gifts?

The purchase amount of a gift bond counts toward the annual limit of the recipient, not the giver. So, in a calendar year, you can buy up to $10,000 in electronic bonds and up to $5,000 in paper bonds for each person you buy for.

Disadvantages

The disadvantages, although minimal are:

- The bonds are Federally taxable

- There is a maximum amount that you can buy

- Minimum term of ownership is one year

- Early redemption penalties if redeemed before 5 years, forfeit interest from the previous 3 months

So if you are looking to boost your yield on some of your cash, and getting more from a bank savings account, certificate of deposit, brokerage cash account, or treasury bond, you should seriously consider a Series I Bond.

How to Invest in Apple Without Buying Apple Stock Plus Get Free Diversification

by Fred Fuld III

Apple (AAPL) has dropped about 18.7% from its high over the last several months. If you think the stock has bottomed out, and may be on the rise, there is an alternative to just buying the stock outright.

No, I’m not talking about stock options. What I’m referring to is Warren Buffett’s Berkshire Hathaway (BRK-A) (BRK-B). Do you realize that Apple makes up 47.6% of the Berkshire Hathaway portfolio?

So if you buy Berkshire, that means that almost half your funds are indirectly invested in Apple.

So what else do you get when you buy Berkshire, besides Warren Buffett’s expertise?

Here are some of the other stocks that make up a large portion of the portfolio:

Bank of America (BAC) 13.5%

American Express (AXP) 7.5%

Coca-Cola (KO) 7.2%

Kraft Heinz (KHC) 3.5%

Moodys (MCO) 2.9%

There are actually over 40 stocks in the Berkshire Hathaway portfolio, spread out over a lot of different industries, so it is well diversified.

I’m not recommending Berkshire as an investment because I think the bear market will continue (and I never make any stock recommendations anyway), but if you are bullish on Apple and you don’t mind a little stock market diversification, you might want to take a look at Berkshire, if not now then at some point when you believe the market has bottomed out.

Disclosure: Author owns AAPL and KO.

Silver as a Hedge Against Inflation: Top Silver Stocks

by Fred Fuld III

Gold and silver have historically been considered a flight to safety, especially during times of high inflation and economic uncertainty. Silver has outpaced inflation during certain time frames.

One of the advantages of silver over gold is that the metal is less expensive, making it more affordable to smaller investors. In addition, silver has far more commercial and industrial uses than gold.

There are several ways to invest in silver. Here are the primary alternatives.

Silver Bullion

You can buy silver bars and rounds in various sizes and weights. They may be produced by the United States government or by private mints. They are easily identifiable and fairly convenient to purchase though coin shops or online gold and silver dealers. You obviously have to be concerned about storage safety do to the potential for theft.

Junk Silver

Junk silver refers to U.S. dimes, quarters, and half dollars minted in 1964 or early, which ere made with 90% silver. These coins have little to no numismatic value, making them a reasonable and simple way of accumulating silver at a reasonable price. Junk silver is available from numerous coin and bullion dealers.

Silver ETF

If you want to invest in silver directly without taking physical ownership, the best way is though a silver exchange traded fund, such as the iShares Silver Trust (SLV). This ETF can be bought and sold just like any stock, without having to worry about storage.

Silver Stocks

There are several companies that specialize in primarily mining for silver. Most of these are Canadian companies, and three of them pay dividends.

First Majestic Silver Corp. (AG), which trades on the NYSE, has a market capitalization of $2.43 billion. The stock has a high trailing price to earnings ratio of 67.7 but a forward P/E ratio of 18.6. Earnings per share for next year are expected to be up 218.8%. The stock pays a small dividend of 0.21%.

Pan American Silver (PAAS) trades on NASDAQ. It has mines in mines in Canada, Mexico, Peru, Argentina, and Bolivia. This $5.24 billion market cap stock trades at 52.6 times trailing earnings and 18.8 times forward earnings. Estimated earnings per share for next year are expected to increase by 35.96%. The company pays a decent dividend yield of 1.97%.

Silvercorp Metals (SVM) is a smaller company, with a market cap of $524.5 million. The company’s mining properties are in China and Mexico. The company has several mines in Mexico, and interests in one mine in Canada. The stock has a very favorable trailing P/E ratio of 15.5, and an a better forward P/E of 10. Just this year, earnings per share jumped by 33%. The dividend for this stock is 1.97%.

Silver Mining ETFs

A diversified way to invest in silver mining companies is through an ETF. The most popular are Global X Silver Miners ETF (SIL), ETFMG Prime Junior Silver Miners ETF (SILJ), and iShares MSCI Global Silver and Metals Miners ETF (SLVP).

Maybe one of these investments may give you a sterling portfolio.

Disclosure: Author didn’t own any of the above at the time the article was written.

Stocks Going Ex Dividend in May 2022

The following is a short list of some of the many stocks going ex dividend during the next month.

Many traders and investors use the stock trading technique called ‘Buying Dividends,’ also commonly referred to as ‘Dividend Capture.’ This is the strategy of buying stocks before the ex dividend date and selling the stock shortly after the ex date at about the same price, yet still being entitled to the dividend.

This technique generally works in bull markets and flat or choppy markets, but you need to avoid the strategy during bear markets. In order to be entitled to the dividend, you have to buy the stock before the ex-dividend date, and you can’t sell the stock until after the ex date.

The actual dividend may not be paid for another few weeks. WallStreetNewsNetwork.com has compiled a downloadable and sortable list of the stocks going ex dividend in the near future. The list contains many dividend paying companies, lots with market caps over $500 million, and some with yields over 2%. Here are a few examples showing the stock symbol, the ex-dividend date, the periodic dividend amount, and the yield.

| Anheuser-Busch Inbev SA (BUD) | 5/3/2022 | 0.407 | 0.95% |

| Levi Strauss & Co (LEVI) | 5/5/2022 | 0.10 | 2.12% |

| Wells Fargo & Company (WFC) | 5/5/2022 | 0.25 | 2.29% |

| Walmart Inc. (WMT) | 5/5/2022 | 0.56 | 1.46% |

| American Electric Power Co. (AEP) | 5/9/2022 | 0.78 | 3.05% |

| Honeywell International Inc. (HON) | 5/12/2022 | 0.98 | 2.06% |

| Starbucks Corporation (SBUX) | 5/12/2022 | 0.49 | 2.63% |

| Charles Schwab Corp (SCHW) | 5/12/2022 | 0.20 | 1.21% |

| Exxon Mobil Corporation (XOM) | 5/12/2022 | 0.88 | 4.13% |

| Amgen Inc. (AMGN) | 5/16/2022 | 1.94 | 3.33% |

| Target Corporation (TGT) | 5/17/2022 | 0.90 | 1.57% |

| Johnson & Johnson (JNJ) | 5/23/2022 | 1.13 | 2.50% |

| The Kraft Heinz Company (KHC) | 5/26/2022 | 0.40 | 3.75% |

| Goldman Sachs Group, Inc. (GS) | 5/31/2022 | 2.00 | 2.62% |

The additional ex-dividend stocks can be found HERE . (If you have been to the page before, and the latest link doesn’t show up, you may have to empty your cache.) If you like dividend stocks, you should check out some of the other high yield stock lists at WSTNN.com HERE .

Dividend definitions:

Declaration date: the day that the company declares that there is going to be an upcoming dividend.

Ex-dividend date: the day on which if you buy the stock, you would not be entitled to that particular dividend; or the first day on which a shareholder can sell the shares and still be entitled to the dividend.

Record date: the day when you must be on the company’s books as a shareholder to receive the dividend. The ex-dividend date is normally set for stocks at two business days before the record date.

Payment date: the day on which the dividend payment is actually made, which can be as long at two months after the ex date.

Don’t forget to reconfirm the ex-dividend date with the company before implementing this technique.

Disclosure: Author did not own any of the above at the time the article was written; affiliate links are on this page.

First Twitter is Taken Over: What Stock is Next?

by Fred Fuld III

I’m sure all of you have heard the news that Elon Musk is buying Twitter (TWTR) for $44 billion at $54.20 per share. What some investors are wondering is if there are any other companies that may be bought out.

Twitter falls into the category of Internet Content & Information. Obviously, some of these stocks are extremely large and unlikely to be bought by anyone or any company. But anything is possible. Plus, with the stock market in general, some of these companies might be reaching a favorable buy range.

The following companies are all Internet Content & Information companies, all are profitable with all but one having price to earnings ratios less than 40, all have sales growth over the last five years in excess of 5%, and all have earnings per share growth this year of over 10%.

| Company | Symbol | Market Cap | P/E |

| Meta Platforms, Inc. | FB | 552.56B | 13.56 |

| Gaia, Inc. | GAIA | 111.99M | 28.78 |

| Alphabet Inc. | GOOGL | 1742.60B | 21.93 |

| Pinterest, Inc. | PINS | 14.23B | 39.14 |

| Shutterstock, Inc. | SSTK | 2.94B | 31.57 |

| Yelp Inc. | YELP | 2.57B | 67.07 |

Keep an eye on these companies during the next few weeks.

Disclosure: Author didn’t own any of the above at the time the article was written.

What Do Investors Care About Today?

What Do Investors Care About Today?

by Ned Raynolds and Art Gormley, The Dilenschneider Group

Excerpted from The Public Relations Handbook copyright © 2022 by Robert L. Dilenschneider. Reprinted with permission from Matt Holt Books, an imprint of BenBella Books, Inc. All rights reserved.

Until recently, investors were concerned almost exclusively about a company’s revenues and earnings lines and where those numbers were headed in the future.

No more.

Today, investors are also becoming increasingly interested in a firm’s positive or negative contributions to society, in a process called ESG investing, standing for Environmental, Social, and Governance concerns.

ESG investing integrates those socially responsible factors into investment analysis and decision making. However, the factors also cover a wide spectrum of issues that are also relevant to an investor’s financial assessment of a company. So, a company’s ability to meet ESG factors may also affect that same bottom line that investors look at first.

According to Forbes, ESG can include:

“how corporations respond to climate change, how good they are with water management, how effective their health and safety policies are in the protection against accidents, how they manage their supply chains, how they treat their workers and whether they have a corporate culture that builds trust and fosters innovation.”

The term “ESG” was coined in 2005 in a landmark study entitled “Who Cares Wins.” According to the most recent calculation, ESG investing is estimated at over $20 trillion in assets under management, about a quarter of all professionally managed assets around the world!

What’s more, ESG investing has become big business. At this writing, many large banks and other money managers had jumped aggressively onto the ESG idea as a way to market their services.

ESG also runs parallel to the more general societal trend today to demand socially responsible behavior from business. To see how far we’ve come, dial back to September 1970, when the legendary economist Milton Friedman wrote an essay for the New York Times entitled, “A Friedman Doctrine: The Social Responsibility of Business Is to Increase Its Profits.” And contrast that with the Business Round table’s August 2019 statement redefining the purpose of a corporation as promoting “an economy that serves all Americans.” It was signed by 181 CEOs “who commit to lead their companies for the benefit of all stakeholders—customers, employees, suppliers, communities and shareholders.”

Because the Roundtable had been considered a bastion of traditional corporate America, that pronouncement received plenty of attention. But the organization’s commitment really builds on what is becoming the current thinking of many business leaders.

Here’s what some of them have said:

- In his 2020 letter to shareholders, Larry Fink, chairman and chief executive of Black Rock, who frequently discussed altruistic issues with the firm’s constituents, wrote, “We are facing the ultimate long-term problem. We don’t yet know which predictions about the climate will be most accurate, nor what effects we have failed to consider. But there is no denying the direction we are heading. Every government, company, and shareholder must confront climate change.”

- Marc Benioff, chair, CEO, and founder of Salesforce, who embraces the title of “activist CEO,” told Fast Company that today, “being a CEO means that you’re taking care of all stakeholders. That stakeholder return is as much table stakes as shareholder return.”

- And Jamie Dimon, chairman and CEO of JPMorgan Chase, who is also chairman of the Business Roundtable, says, “The American dream is alive, but fraying. Major employers are investing in their workers and communities because they know it is the only way to be successful over the long term. These modernized principles reflect the business community’s unwavering commitment to continue to push for an economy that serves all Americans.”

Further endorsement of ESG principles comes from an unexpected source— the Vatican. The Council for Inclusive Capitalism is affiliated with the Catholic Church and operates under “the moral guidance of Pope Francis.” The Council also includes CEOs of several Fortune 500 companies as well as policymakers and the general secretary of the International Trade Union Confederation. The founder of the Council, Lynn Forester de Rothschild, also chair of investment firm E. L. Rothschild, said, “Doing this is not simply a market imperative . . . The capital markets are such a powerful force, that we need to remember that our actions, who we are and what we are, are based on morality and ethics. And so the Holy Father really asks us to put profits in service of planet and people.”

What are enlightened companies doing today to let investors know about their ESG commitments? Here are some steps to consider:

- In the annual Form 10-K, include a section summarizing the company’s ESG actions.

- Issue an annual Sustainability Report, as a number of companies today are doing, especially those with environmental vulnerabilities.

- Weave material on ESG compliance into earnings news releases and periodically include reports on ESG actions in quarterly earnings presentations.

The above is excerpted from The Public Relations Handbook

About the Editor of The Public Relations Handbook:

Robert L. Dilenschneider formed The Dilenschneider Group in October, 1991. Headquartered in New York and Chicago, the Firm provides strategic advice and counsel to Fortune 500 companies and leading families and individuals around the world, with experience in fields ranging from mergers and acquisitions and crisis communications to marketing, government affairs and international media.

Prior to forming his own firm, Dilenschneider served as president and chief executive officer of Hill and Knowlton, Inc. from 1986 to 1991, tripling that Firm’s revenues to nearly $200 million and delivering more than $30 million in profit. Dilenschneider was with that organization for nearly 25 years. Dilenschneider started in public relations in 1967 in New York, shortly after receiving an MA in journalism from Ohio State University, and a BA from the University of Notre Dame. For more information, please visit https://robertldilenschneider.com

About the Authors:

Ned Raynolds is a veteran corporate communications executive and strategic advisor with more than thirty years’ experience, versed in all phases of external and internal communications. His focus is on positioning companies that are facing serious challenges with the news media, employees, customers, and the investment community, often working in a team approach with senior management, legal counsel, and outside advisors. Mr. Raynolds previously managed corporate communications for American Airlines for the East Coast, including New York, Boston, and Washington, DC. At American, he enlisted specialty media to reach nearly half a million high-value consumers in Greater New York.

Art Gormley, a Principal with The Dilenschneider Group, joined the firm in 1992, shortly after it was founded. He oversees the firm’s financial relations practice and has worked with the Wall Street and international investment communities for more than twenty-five years. Mr. Gormley has counseled the chief executives, chief financial officers, and boards of directors of countless clients, including some of the world’s largest publicly held corporations. In addition, Mr. Gormley is a highly experienced crisis communicator who has guided clients in their dealings with financial restatements, shareholder litigation, activist investors, and management changes, as well as investigations involving the Securities and Exchange Commission, Internal Revenue Service, and the US Department of Justice, among other government agencies. For more information, please visit https://www.dilenschneider.com

How to Hedge Your Portfolio Against Skyrocketing Food Prices

by Fred Fuld III

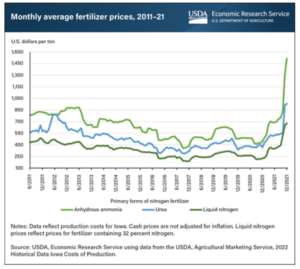

Did you know that fertilizer prices spiked in the U.S. market in late 2021, just ahead of 2022 planting season, according to the United States Department of Agriculture? This was before Russia invaded Ukraine.

Now, because of the Russian / Ukraine War, prices will continue to rise, since Russia produces almost ten million metric tons of nitrogen fertilizer per year, the fourth largest producer in the world.

Higher Fertilizer Prices

With higher fertilizer prices, you get higher, wheat, corn, and soybean prices. With higher wheat, corn, and soybean prices, you get higher food prices in general. And you can also get food shortages as well.

Higher Food Prices

I recently wrote about the soaring prices of items on Amazon, called The Amazon Inflation Rate is Running at 68% Per Year, and showed that many of these increases were due to food items. I described how dark chocolate candy rose by 148%, light tuna in water by 28%, multi-seed cheesy garlic crackers by 194%, sesame bars with honey and almonds by 134%, and on and on. This was all during a twelve month period ending last November, and remember, this was before the war.

So what is an investor to do?

If you are willing to take a lot of risk, you can trade the futures market. But for those that prefer to stick with stocks and ETFs, there are still opportunities.

Individual Agricultural Funds

One way is by buying agricultural commodities exchange traded funds. There are ETFs and ETNs available for corn, wheat, soybeans, and several other ag products.

The Teucrium Corn Fund (CORN), which invests in corn futures, has a market cap of $222 million, an expense ratio of 1.76%, and is up 29.79% year to date.

The Teucrium Wheat Fund (WEAT) has net assets of $493 million. It has an expense ratio of 1.00%, and year-to-date is up 38%.

The Teucrium Soybean Fund (SOYB) has a market cap of $64 million, an expense ratio of 1.16%, and is up 21.18% year to date.

Diversified Agricultural Funds

If you prefer to reduce your risk through diversification, you might want to consider Invesco DB Agriculture Fund (DBA), which invests in a basket of agricultural commodities futures. The market cap is $1.85 billion, the expense ratio is 0.85%, and the year-to-date total return is 11.2%.

Another diversified investment is the Elements Rogers International Commodity Index-Agriculture Total Return ETN (RJA), which is up 17.98% so far this year. The market cap is $153 million and the expense ratio is 0.75%.

Most of these funds are very volatile, very speculative, and can have low volume and very wide spreads.

Maybe one of these will help you offset the prices you pay at the supermarket.

Disclosure: Author didn’t own any of the above at the time the article was written but plans to put on a bullish option spread on CORN in the next few days.