If you are looking for some great reading for the holidays, or maybe a great gift for your investor friends and relatives, here are some books on financial scams that are well worth reading. Many of these came out a few years go, but are timeless. Enjoy!

American Kingpin: The Epic Hunt for the Criminal Mastermind Behind the Silk Road by Nick Bilton You have probably heard of the Silk Road but do you know anything about the guy behind it? How he started it, how it grew beyond his or anyone’s wildest dreams, and how money and power can corrupt. It also corrupted some members of law enforcement. An amazing story and a book that reads like a page-turner mystery.

Billion Dollar Whale: The Man Who Fooled Wall Street, Hollywood, and the World by Tom Wright & Bradley Hope If you have seen the Wolf of Wall Street movie, but you don’t know where the money came from to make the movie, you need to read this book! How billions were swindled with the help of a major investment banking company. The parties were unbelievable, and included such guests as Leonardo DiCaprio and Paris Hilton. The jewelry was unbelievable. The yachts were unbelievable.

Alligator Blood by James Leighton An Australian in his 20s goes from delivering pizzas to becoming one of the richest people in Australia from online poker. What happens next …

The Beneish M-Score is a financial metric designed to identify the likelihood that a company has engaged in earnings manipulation. Developed by Professor Messod Beneish of Indiana University, the M-Score uses a combination of financial ratios and variables to flag irregularities in accounting practices. Since its introduction in the late 1990s, it has become a critical tool for auditors, investors, and analysts who aim to evaluate the authenticity of a company’s financial reporting.

At its core, the Beneish M-Score combines eight variables, derived from publicly available financial statements, to create a composite score. These variables include metrics like the Days Sales in Receivables Index (DSRI), which measures changes in the relationship between receivables and sales, and the Gross Margin Index (GMI), which compares a company’s gross margin over time. Others, like the Asset Quality Index (AQI) and the Total Accruals to Total Assets Ratio (TATA), further analyze a firm’s asset structure and discretionary accounting practices.

The calculation results in a score that typically falls into one of two categories: firms with an M-Score less than -2.22 are considered less likely to manipulate earnings, while those with an M-Score higher than this threshold warrant further scrutiny.

I want to make sure you understand completely how this score works. It is always calculated as a negative number. The lower the negative number, the less likely the accounting is being manipulated. The higher the number, in other words, the smaller the negative number, the chances are greater that manipulation is involved.

A rule of thumb is that if the M-Score is -2.00 or lower, a greater NEGATIVE number, such as -2.50 or -3.00, the company is not a manipulator. If the score falls into the range of -2.00 to -1.78, the company is a possible manipulator. If the score is -1.78 to zero, it is a likely manipulator.

Although the M-Score does not definitively prove manipulation, it raises red flags, signaling that a company’s financial activities may require deeper investigation.

One of the most famous cases illustrating the power of the Beneish M-Score involved Enron. Retrospective analyses revealed that the M-Score flagged the company as a high-risk manipulator well before its infamous collapse. This case demonstrated the score’s potential as a forward-looking tool, though it also highlighted its reliance on accurate and consistent data from company filings.

Despite its utility, the Beneish M-Score has limitations. It is primarily designed for manufacturing or industrial firms and may be less effective in service-oriented or financial sectors, where the nature of financial reporting differs significantly. Furthermore, the M-Score is sensitive to accounting anomalies, which may not necessarily indicate deliberate manipulation but rather reflect differences in industry practices, acquisitions, or rapid growth.

For investors and analysts, the Beneish M-Score should be viewed as a starting point rather than a definitive verdict. It is most effective when used alongside other analytical tools and qualitative assessments. When combined with careful evaluation of a company’s leadership, industry trends, and broader financial metrics, the M-Score can serve as a valuable part of a due diligence process.

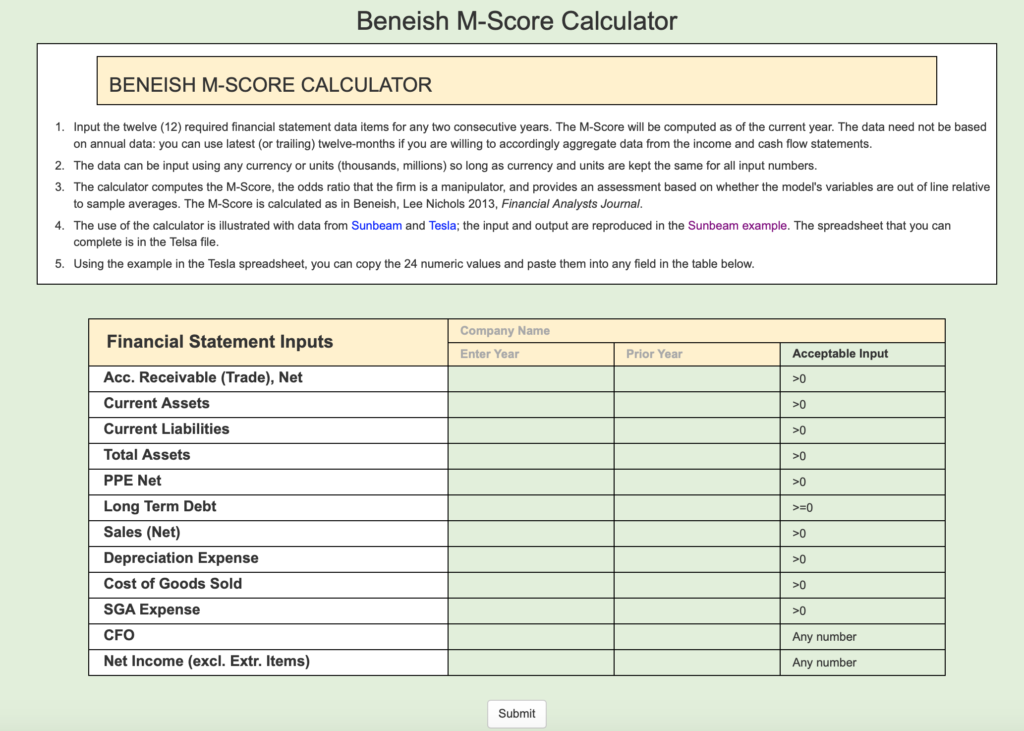

If you want to try the M-Score on a stock you are interested in, you can go to the M-Score Calculator, which is hosted by Indiana University, and try it on your own.

I tried it with a couple of stocks and this is what I came up with.

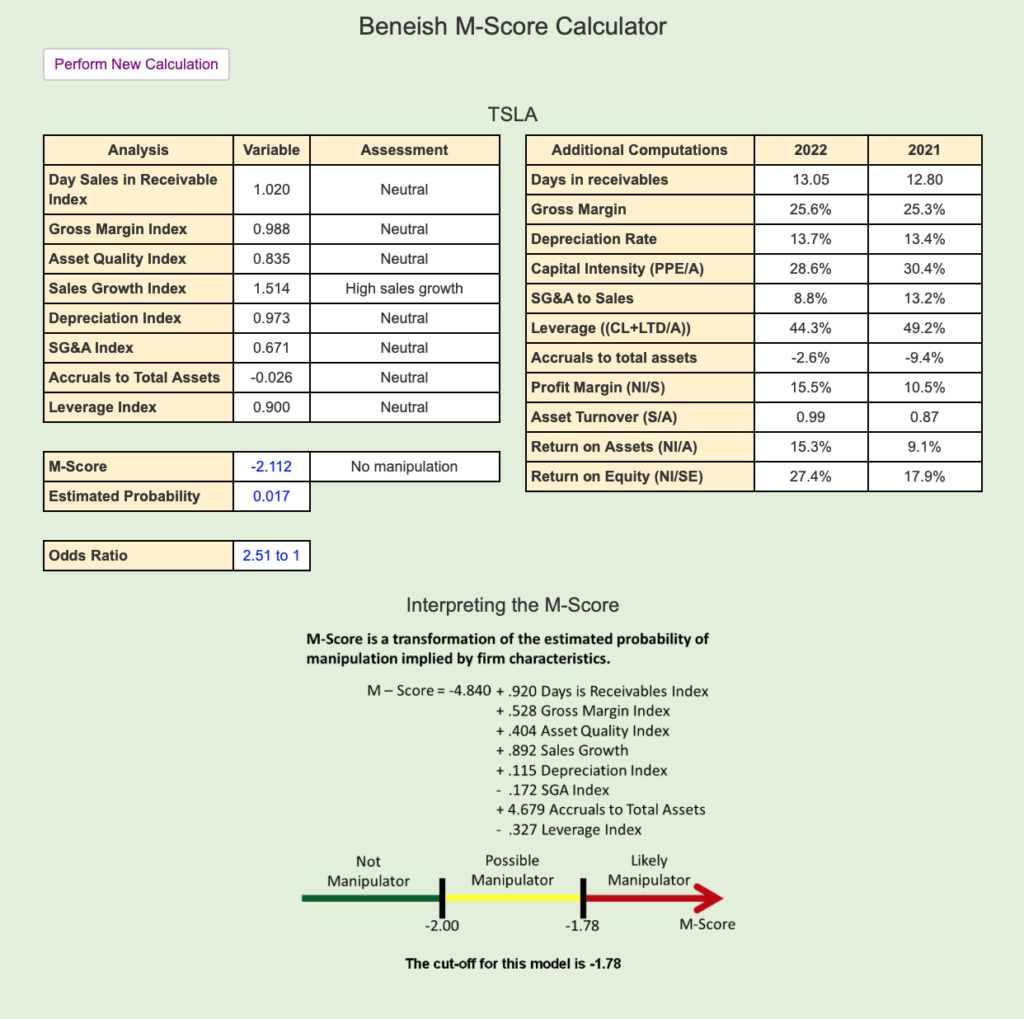

First, I started with Tesla (TSLA).

Tesla ended up with an M-Score of -2.112, a score of less than -2.00 (a greater negative number that -2.00), which means it falls in the green Not a Manipulator category.

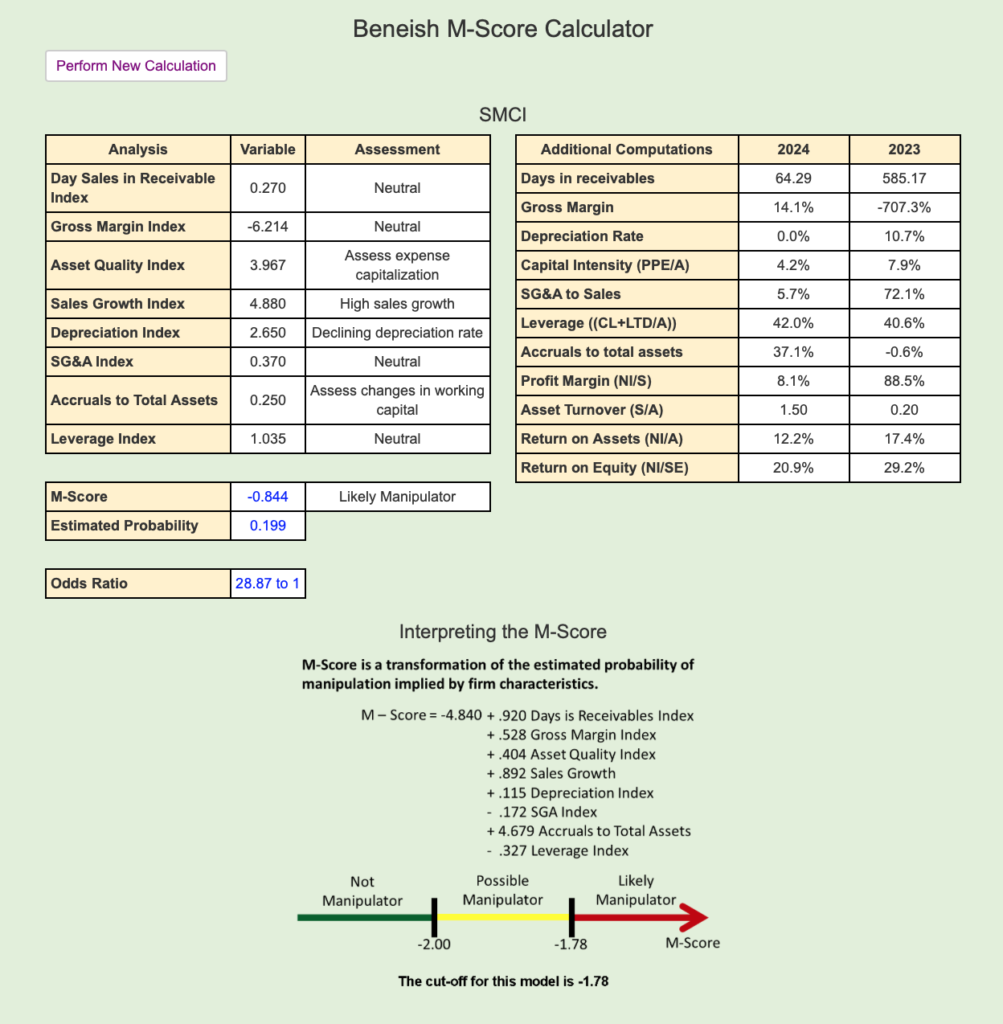

Then I tried Super Micro Computer (SMCI):

You have probably seen the news lately about SNCI.

Accounting Firm Resignation: In October 2024, Ernst & Young resigned as Super Micro’s auditor, citing concerns about transparency and internal controls related to financial reporting.

Delayed Annual Report: Super Micro delayed the filing of its annual report, leading to a significant drop in its stock price.

Hindenburg Research Report: Hindenburg Research published a report alleging that Super Micro continued to engage in accounting manipulation, sibling self-dealing, and potential sanctions evasion.

These recent events have raised serious concerns about the accuracy and reliability of Super Micro’s financial reporting. Investors and analysts are closely monitoring the situation as the company works to address these issues and regain credibility.

So what did the M-Score Calculator show for Super Micro? It displayed an M-Score of -0.844, a higher number than -1.78 (lower negative number), based on the. This puts it well in the range of red Likely Manipulator.

In today’s complex financial landscape, where trust in corporate reporting is paramount, tools like the Beneish M-Score play a crucial role. By offering a quantitative approach to identifying irregularities, it empowers stakeholders to make informed decisions, promoting greater accountability in corporate governance.

If you are looking for some springtime reading, then books about financial swindles, scandals, and scams should interest you. All these books are non-fiction, the real thing, and provide true stories that are pretty incredible.

I have real all of these books, except the last one, and I highly recommend all of them. Enjoy.

American Kingpin: The Epic Hunt for the Criminal Mastermind Behind the Silk Road by Nick Bilton

You have probably heard of the Silk Road but do you know anything about the guy behind it? How he started it, how it grew beyond his or anyone’s wildest dreams, and how money and power can corrupt. It also corrupted some members of law enforcement. An amazing story and a book that reads like a page-turner mystery.

Billion Dollar Whale: The Man Who Fooled Wall Street, Hollywood, and the World by Tom Wright & Bradley Hope

If you have seen the Wolf of Wall Street movie, but you don’t know where the money came from to make the movie, you need to read this book! How billions were swindled with the help of a major investment banking company. The parties were unbelievable, and included such guests as Leonardo DiCaprio and Paris Hilton. The jewelry was unbelievable. The yachts were unbelievable.

Alligator Blood by James Leighton

An Australian in his 20s goes from delivering pizzas to becoming one of the richest people in Australia from online poker. What happens next …

One of the directors of BitConnect, Glenn Arcaro, has pleaded guilty to wire fraud conspiracy for his role in the BitConnect scam, according to the U.S. Department of Justice.

BitConnect went out of business in 2018. Prosecutors said that the company was “a textbook Ponzi scheme”. The DoJ said investors lost over $2 billion in the fraud.

Bitconnect was created in 2016 with the goal of allowing users to lend the value of the Bitconnect coin in return for interest payments.

The BitConnect coin, known as BCC, rose from a post ICO price of $0.17 to an all-time high of $463 in December 2017; it tanked to $0.40 as in March of 2019.

Company Will Pay $62 Million to Settle Charges Related to Inflated Cost Savings that Caused it to Restate Several Years of Financial Reporting

FOR IMMEDIATE RELEASE

2021-174

Washington D.C., Sept. 3, 2021 —

The Securities and Exchange Commission today charged The Kraft Heinz Company (KHC) with engaging in a long-running expense management scheme that resulted in the restatement of several years of financial reporting. The SEC also charged Kraft’s former Chief Operating Officer Eduardo Pelleissone and its former Chief Procurement Officer Klaus Hofmann for their misconduct related to the scheme.

According to the SEC’s order, from the last quarter of 2015 to the end of 2018, Kraft engaged in various types of accounting misconduct, including recognizing unearned discounts from suppliers and maintaining false and misleading supplier contracts, which improperly reduced the company’s cost of goods sold and allegedly achieved “cost savings.” Kraft, in turn, touted these purported savings to the market, which were widely covered by financial analysts. The accounting improprieties resulted in Kraft reporting inflated adjusted “EBITDA,” a key earnings performance metric for investors. In June 2019, after the SEC investigation commenced, Kraft restated its financials, correcting a total of $208 million in improperly-recognized cost savings arising out of nearly 300 transactions.

“Investors rely on public companies to be 100% truthful and accurate in their public statements, especially when it comes to their financials. When they fall short in this regard, we will hold them accountable,” said Gurbir S. Grewal, Director of the SEC’s Division of Enforcement. “Today’s action demonstrates that no matter how complex and far-reaching the financial misconduct, we will vigorously pursue wrongdoers because that’s what investor protection requires.”

As alleged in the SEC’s order and in its complaint against Hofmann, Kraft failed to design and maintain effective internal accounting controls for its procurement division. As a result, finance and gatekeeping personnel repeatedly overlooked indications that expenses were being improperly accounted for. In addition, Pelleissone was presented with numerous warning signs that expenses were being managed through manipulated agreements with Kraft’s suppliers, but rather than addressing these risks, he pressured the procurement division to deliver unrealistic savings targets. Hofmann approved several improper supplier contracts used to further the misconduct despite numerous warning signs that procurement division employees were circumventing internal controls, and certified the accuracy and completeness of the procurement division’s financial statements when the misconduct was occurring. As a member of Kraft’s disclosure committee, Pelleissone then improperly approved the company’s financial statements.

“Kraft and its former executives are charged with engaging in improper expense management practices that spanned many years and involved numerous misleading transactions, millions in bogus cost savings, and a pervasive breakdown in accounting controls. The violations harmed investors who ultimately bore the costs and burdens of a restatement and delayed financial reporting,” said Anita B. Bandy, Associate Director of the SEC’s Division of Enforcement. “Kraft and its former executives are being held accountable for placing the pursuit of cost savings above compliance with the law.”

The SEC’s order finds that Kraft violated the negligence-based anti-fraud, reporting, books and records, and internal accounting controls provisions of the federal securities laws. The order also finds that Pelleissone violated the negligence-based anti-fraud, books and records, and internal accounting controls provisions of the federal securities laws and additionally, failed to provide Kraft’s accountants with accurate information and caused Kraft’s reporting, books and records, and internal accounting controls violations. The SEC’s complaint against Hofmann alleges that he violated the negligence-based anti-fraud provisions, failed to provide accurate information to accountants, and violated the books and records and internal accounting controls provisions of the federal securities laws.

Without admitting or denying the SEC’s findings as to them, Kraft consented to cease and desist from future violations and pay a civil penalty of $62 million, whereas Pelleissone consented to cease and desist from future violations, pay disgorgement and prejudgment interest of $14,211.31, and pay a civil penalty of $300,000. And without admitting or denying the SEC’s allegations, Hofmann consented to a final judgment permanently enjoining him from future violations, ordering him to pay a civil penalty of $100,000, and barring him from serving as an officer or director of a public company for five years. The settlement with Hofmann is subject to court approval.

The SEC’s investigation was conducted by Seth M. Nadler, Thomas B. Rogers, James Connor, Gary Peters, with assistance from Sarah Concannon and Thomas Bednar, and was supervised by Greg Faragasso and Ms. Bandy.

Do you know what all of the following have in common (in no particular order)?

Paris Hilton

Leonardo Dicaprio

Martin Scorsese

Malasia

Swiss Banks

Kleptocracy

Wolf of Wall Street Movie

Hollywood

Wall Street

Goldman Sachs

$500,000,000 Yacht

Miranda Kerr

$325,000 Ferrari

Supermodels

$33.5 million Manhattan condominium

President Obama

President Trump

Jamie Foxx

Busta Rhymes

Kasseem Dean

Alicia Keys

Swizz Beatz

Money Laundering

Cyprus

China

Macau

Indonesia

Bali

United States

12,000 pieces of jewelry

567 handbags

423 watches

FBI

Casinos

Million dollar parties

Las Vegas

All of the above are connected to a man named Jho Low, a Malaysian businessman who is accused of swindling billions of dollars, indirectly from the Malaysian government, and spending it on huge parties with actors, models, numerous bottles of champagne, gambling, and entertainment, in addition to expensive homes around the world.

Ironically, according to the book, Low funded the Martin Scorsese movie The Wolf of Wall Street, starring Leonardo DiCaprio, which was based on the true story of Jordan Belfort, the convicted stock market manipulator and boiler-room operator.

The story of Low reads like a financial mystery and thriller, and I rarely say this about a non-fiction book, but it is a page-turner.

So if you are looking for some end of summer reading, and if you like to read about frauds, scams, and swindles, Billion Dollar Whale will definitely keep you occupied.

Would you believe that crooks are actually creating fake broker-dealers in order to swindle you out of your money? In the old days, con men would set up real brokerage firms, then either churn your account, push penny stock pump-and-dump stocks on you, or on rare occasions, sell you totally fraudulent tax shelters.

But now, fictitious brokers and investment adviser companies are being created and many have names that sound like legitimate firms.

The Securities and Exchange Commission has a listing of a whole bunch of these scams. One interesting thing to note is that 28 of these firms are from New York, whereas only three are from California.

In the “old days,” most of the scams worked out of Newport Beach and Century City in California. I guess these days, New York adds more legitimacy to an investment company.

Plus, some companies claim to be registered with an “official” United States agencies, that are either fake or pretend to be part of the U. S. Government. This is a list of fictitious governmental agencies.

If you have any doubt about a firm that you are planning on doing business with, check them out.