by Fred Fuld III

While the “one-dollar CEO” was once a popular trend among Silicon Valley elite (like Larry Page and Mark Zuckerberg), it has become a rarer breed in the 2020s. Most CEOs who famously took $1 salaries have either stepped down or shifted their compensation structures.

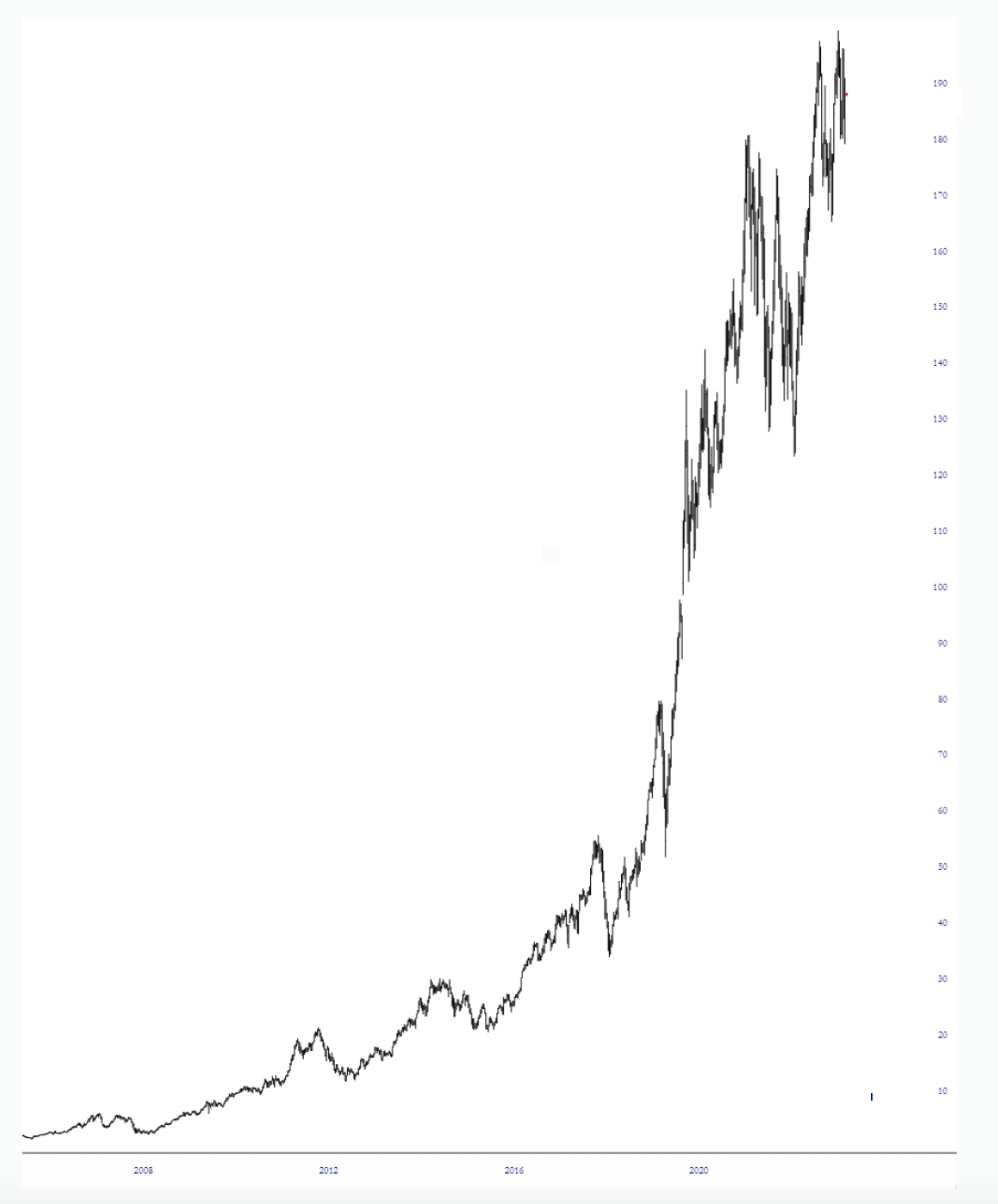

Steve Jobs is often credited with popularizing the modern “$1 CEO” trend. After rejoining Apple in 1997, he famously took a $1 annual salary for 14 years until his resignation in 2011.

While his salary was a single dollar, his performance—and the stock’s performance—was anything but nominal.

Apple’s Performance Under the $1 Salary (1997–2011)

When Jobs returned, Apple was weeks away from bankruptcy and trading at split-adjusted prices that are today measured in pennies. By the time he stepped down, he had transformed it into the most valuable company in the world.

- Stock Growth: Apple’s stock (AAPL) grew by approximately 6,700% during his tenure.

- vs. S&P 500: During that same period, the S&P 500 returned roughly 4.5% per year (heavily suppressed by the Dot-com bubble burst and the 2008 Financial Crisis). Apple averaged a staggering 33.6% annual return.

- Revenue: Apple’s annual revenue exploded from $7.1 billion in 1997 to $108.2 billion in 2011.

Was he actually only making $1?

While the salary was symbolic, Jobs was compensated in other massive ways that aligned his wealth with the company’s success:

- Massive Stock Ownership: Jobs held about 5.5 million shares of Apple. He didn’t sell a single share between 1997 and 2011, meaning his “paycheck” was effectively the billions of dollars in value added to his holdings.

- The “Bonus” Jet: In 1999, Apple’s board gave him a $90 million Gulfstream V private jet and reimbursed him for all expenses related to it.

- Disney Stock: Jobs was also the largest individual shareholder of Disney (following the sale of Pixar), which paid him millions in dividends annually—far more than any CEO salary could.

The Verdict on the $1 Salary

Jobs is the ultimate success story for this model because his $1 salary signaled a “sink or swim with the shareholders” mentality. He took the dollar when the company was failing to prove his commitment, and he kept it when the company was winning to show that his motivation was the product, not the cash.

Most modern CEOs who try this (as seen in the 2025 performance data) haven’t quite managed to replicate that “Jobs Magic” in terms of raw market outperformance.

However, a few notable examples still exist or have recently committed to this path. Here is how they and their stocks have fared over the last year (ending early 2026) compared to the S&P 500, which returned approximately 16.3% in 2025.

The $1 CEO Club: Performance vs. S&P 500

| Company | CEO | 2025 Stock Performance | vs. S&P 500 (+16.3%) |

| Tesla (TSLA) | Elon Musk | +19% | Outperformed |

| Airbnb (ABNB) | Brian Chesky | ~ -5% | Underperformed |

| Yelp (YELP) | Jeremy Stoppelman | -32% | Underperformed |

| Gloo (GLOO) | Scott Beck | N/A (New for 2026) | N/A |

Key Company Breakdowns

- Tesla (TSLA): Elon Musk remains the most famous member of this group. While his base salary is $0 (or the California minimum wage, which he does not accept), his actual compensation is tied to massive performance-based stock options. In 2025, Tesla’s stock was a roller coaster—dropping significantly in Q1 before rallying on the launch of its robotaxi network to end the year up 19%, slightly beating the broader market.

- Yelp (YELP): Jeremy Stoppelman has maintained a $1 salary for years. Unfortunately for shareholders, 2025 was a difficult year for Yelp. Despite high gross margins, the stock tumbled 32% over the last year as it struggled with slower customer spending and a transition toward AI-driven local commerce services.

- Airbnb (ABNB): Brian Chesky famously reduced his salary to $1 during the pandemic. While he receives other forms of compensation (like security and travel), his base remains nominal. The stock saw modest volatility in 2025, ending the year down roughly 5% as the travel sector normalized after the post-pandemic boom.

- Gloo (GLOO): A newer entry to the list, Gloo announced that its CEO Scott Beck would slash his salary to $1 starting in February 2026 to signal confidence in the company’s “faith-tech” platform despite recent net losses.

Is the “$1 Salary” a Good Sign for Investors?

The data suggests that a $1 salary is not a guarantee of stock success. While it aligns the CEO’s wealth with shareholders, it often indicates that the executive is already a billionaire (like Musk or Chesky) or that the company is going through a “turnaround” phase where cash preservation is critical. In 2025, the $1 CEO group largely underperformed the S&P 500, with Tesla being the lone standout.

Disclosure: Author owns AAPL and TSLA. No investment recommendations are expressed or implied.